Table of Contents

ToggleKey Takeaways

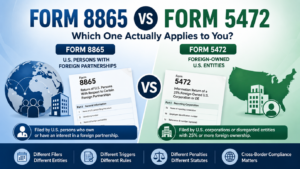

- Form 5472: foreign-owned U.S. entities. Form 8865: U.S. persons with foreign partnerships. Different filers.

- If a U.S. person owns/controls interest in a foreign partnership, Form 8865 may be required — not Form 5472.

- Form 8865 has 4 categories of filers, each with different ownership thresholds.

- Form 8865 penalty: $10,000 per failure per partnership per year, plus continuation penalties.

- You can have both Form 5472 and Form 8865 if structure includes both U.S. entities with foreign owners and foreign entities with U.S. owners.

- U.S. expats are the most common Form 8865 filers — and the most common to miss it.

Where This Post Fits

→ What Is Form 5472? (pillar) (/knowledge/what-is-form-5472)

→ Do Partnerships Need to File Form 5472? (/knowledge/do-partnerships-file-form-5472)

Globally mobile founders, U.S. expats, and cross-border investors frequently run into confusion when comparing these two international information returns. Many hear “foreign business reporting” and assume Form 5472 applies automatically. In practice, the correct filing obligation is often Form 8865 instead.

Understanding which IRS international information return applies is critical because filing the wrong form — or missing the required filing entirely — can trigger substantial IRS penalties.

The Two Forms in One Sentence

Form 5472: reports related-party transactions of a 25% foreign-owned U.S. corporation/disregarded entity.

Form 8865: reports a U.S. person’s interest in a foreign partnership.

Different filer. Different entity. Different country. Different statute (§ 6038A vs §§ 6038/6038B/6046A).

Side-by-Side Comparison

| Feature | Form 5472 | Form 8865 |

| Who files | U.S. corporation or DE | U.S. person |

| Entity reported | U.S. entity with foreign ownership | Foreign partnership |

| Trigger | 25%+ foreign ownership + reportable transactions | Specific ownership/control thresholds |

| Statute | IRC § 6038A | IRC §§ 6038, 6038B, 6046A |

| Filed with | Pro forma Form 1120 | U.S. person’s own income tax return |

| E-file allowed | No (foreign-owned DEs) | Yes (with underlying return) |

| Base penalty | $25,000 per related party per year | $10,000 per partnership per year |

| Continuation | $25,000 per 30 days (no cap) | $10,000 per 30 days (capped at $50,000) |

The Four Categories of Form 8865 Filers

| Category | Who | What Triggers |

| Category 1 | U.S. person with controlling interest >50% | Owns >50% any time during partnership year |

| Category 2 | U.S. person with 10%+ interest in U.S.-controlled partnership | Foreign partnership has U.S. partners owning >50% |

| Category 3 | U.S. person who contributed property | Contribution where U.S. owns 10%+ after, OR exceeds $100K |

| Category 4 | U.S. person with reportable changes | Acquisition/disposition of 10%+ interest, or threshold crossings |

Common Scenarios

U.S. Citizen Living Abroad with a Foreign LLC

An American expat in Singapore owns 100% of a Pte Ltd treated as a foreign partnership for U.S. tax purposes. Form 8865 (Category 1) generally applies — not Form 5472.

Non-U.S. Founder with U.S. LLC

A U.K. resident owns 100% of a U.S. single-member LLC. Form 5472 applies — not Form 8865.

Both Forms Apply

A U.S. citizen owns a U.S. LLC with a foreign parent and also owns an interest in a foreign partnership in another country. Both forms apply — separate filings, separate reporting requirements, and separate deadlines.

Worked Example: A U.S. Expat With a Singapore Pte Ltd

Facts: A U.S. citizen living in Singapore owns 100% of a Pte Ltd that elects (or defaults) to partnership treatment for U.S. tax purposes under Treas. Reg. § 301.7701-3. In 2025, the Pte Ltd has $500,000 of gross revenue, $120,000 of net income, and the owner contributes an additional $75,000 of cash to the partnership mid-year.

Analysis

- The owner is a Category 1 filer (controlling >50% interest at any time during the partnership year).

- The $75,000 cash contribution triggers Category 3 reporting on Schedule O under IRC § 6038B (any contribution where the U.S. person owns 10% or more after the transfer, or where contributions exceed $100,000 in the year).

- The owner files one Form 8865 covering both categories — not two separate Form 8865s — attached to the owner’s Form 1040.

- Form 5472 is not required. The Pte Ltd is a foreign entity owned by a U.S. person, not a U.S. entity owned by a foreign person.

- Likely additional filings: FBAR (FinCEN 114) for the Singapore bank account if aggregate foreign account balances exceed $10,000; Form 8938 with the Form 1040 if asset thresholds are met; Form 5471 is not required because the entity is a partnership, not a corporation.

Penalty exposure if missed: $10,000 for Category 1 + 10% of the $75,000 contribution ($7,500) for Category 3 = $17,500 minimum, before continuation penalties and foreign-tax-credit reductions. A single overlooked Form 8865 can equal 15–20% of the entity’s net income.

Filing Mechanics: How and When Each Form Is Filed

- Form 8865 is filed with the U.S. person’s income tax return (Form 1040 for individuals, Form 1120 for corporations, Form 1065 for partnerships). It is e-filed when the underlying return is e-filed. Due date follows the underlying return: generally April 15 for individuals, with automatic extensions available via Form 4868 (individuals) or Form 7004 (entities).

- Form 5472 is filed with a pro forma Form 1120 by foreign-owned U.S. disregarded entities. It must be paper-filed or faxed (not e-filed) to the IRS service center in Ogden, Utah. Due date is April 15 for calendar-year filers, with extension via Form 7004.

- Schedules required with Form 8865 vary by category: Schedule A (constructive ownership), Schedule B (income statement), Schedule K and K-1 (partner shares), Schedule L (balance sheet), Schedule M (balance sheet reconciliation), Schedule M-1 (book-tax reconciliation), Schedule M-2 (partner capital), Schedule N (related-party transactions), Schedule O (contributions — Category 3 only), and Schedule P (acquisitions/dispositions — Category 4 only).

What is Schedule O on Form 8865?

Schedule O reports property contributions by a U.S. person to a foreign partnership under IRC § 6038B. It is required for Category 3 filers when the U.S. person owns 10% or more of the partnership after the contribution, or when contributions during the year exceed $100,000. Missing Schedule O carries a separate 10% penalty on the contribution amount (capped at $100,000, uncapped if intentional).

Does owning a foreign LLC always require Form 8865?

No. Form 8865 applies only when the foreign entity is treated as a partnership for U.S. tax purposes. If the foreign LLC is a disregarded entity (single-member), Form 8858 may apply instead. If it is treated as a corporation — either by default or by Form 8832 election — Form 5471 typically applies. Entity classification under Treas. Reg. § 301.7701-3 controls which form is required.

Form 8865 Penalties — Why This Matters

- $10,000 per failure to file per partnership per year.

- Plus 10% reduction in foreign tax credits attributable to the partnership.

- Continuation: $10,000 per 30-day period, capped at $50,000.

- Failure to report contributions (Category 3): 10% of contribution amount, capped at $100,000 (no cap if intentional).

In the broader penalty discussion, many taxpayers underestimate Form 8865 penalties because Form 5472 receives more attention online. In reality, Form 8865 penalties can become extremely expensive for expats and international business owners with multi-year noncompliance.

Where DIY Filings Most Often Go Wrong

- Filing Form 5472 because founder heard “foreign business” when Form 8865 was actual requirement.

- Missing Form 8865 entirely because U.S. tax preparers focus on domestic return.

- Filing one category but missing others (Category 1 often is also Category 4).

- Not filing Schedule O (transfers under § 6038B).

- Treating foreign LLC as automatically a corporation when it should default to partnership.

- Missing FBAR and Form 8938 alongside Form 8865.

- Not coordinating Form 8865 with U.S. partner’s Form 1040.

When Professional Preparation Is Strongly Recommended

- Any U.S. person with interest in foreign partnership/LLC.

- U.S. expats with foreign business interests.

- Property contributions to foreign partnerships.

- Ownership crossing 10%, 25%, 50%, 75% thresholds.

- Unsure whether foreign entity is partnership or corporation for U.S. tax purposes.

- Multi-year missed Form 8865 filings.

Cross-border entity classification rules can be highly technical, especially when foreign LLCs default to partnership treatment under U.S. tax regulations. Proper classification directly affects whether the filing requirement falls under Form 8865, Form 5472, Form 1065, or other international reporting regimes.

Frequently Asked Questions

What is the difference between Form 5472 and Form 8865?

The core distinction is the entity being reported. Form 5472 is filed by U.S. entities with foreign owners, while Form 8865 is filed by U.S. persons with interests in foreign partnerships.

I am a U.S. expat — do I file Form 5472 or Form 8865?

Generally Form 8865 if there is an interest in a foreign partnership, plus possibly FBAR and Form 8938.

What is the penalty for missing Form 8865?

$10,000 per partnership per year, plus 10% reduction in foreign tax credits, plus continuation penalties up to $50,000.

Can one person file both Form 5472 and Form 8865?

Yes. Separate filings for separate entities.

When is Form 8865 due?

With the U.S. person’s income tax return — generally April 15 for individuals, with extensions available where applicable.

The Bottom Line

In most cases, the deciding factor is the direction of ownership:

Foreign owner → U.S. entity = Form 5472.

U.S. person → foreign partnership = Form 8865.

Understanding that distinction early can prevent major compliance mistakes, missed filings, and unnecessary IRS penalties.

Need Help Untangling Form 5472 vs 8865?

Optimize Tax LLC handles cross-border filings every season for U.S. expats and foreign-owned U.S. businesses — Form 5472, Form 8865 (all four categories), Schedule O property-contribution reporting, FBAR (FinCEN 114), Form 8938, and coordinated Form 1040 / 1040-NR / 1120-F preparation under §§ 6038, 6038A, 6038B, and 6046A.

If you have a foreign partnership interest or a foreign-owned U.S. entity, schedule a consultation with a credentialed CPA and EA at Optimize Tax.

Continue Reading: The Form 5472 Knowledge Series

- What Is Form 5472? A Plain-English Guide for Foreign-Owned LLCs (pillar) (/knowledge/what-is-form-5472)

- Do You Need an EIN for a Foreign-Owned LLC? (/knowledge/ein-foreign-owned-llc)

- Form 8832 Entity Classification Election (/knowledge/form-8832-entity-classification)

- Do I Need to File Form 5472 If My LLC Had No Activity? (/knowledge/form-5472-no-activity)

- How to File Taxes for a Foreign-Owned Single-Member LLC (2026) (/knowledge/foreign-owned-smllc-tax-filing)

- What Is a Form 1120 Pro Forma? (/knowledge/form-1120-pro-forma)

- Do Partnerships Need to File Form 5472? (/knowledge/do-partnerships-file-form-5472)

- Foreign-Owned Multi-Member LLCs: Form 1065 + 8805 (/knowledge/foreign-owned-multi-member-llc-form-1065-8805)

- Schedules K-2 and K-3: International Reporting for Partnerships (/knowledge/schedules-k2-k3-partnerships)

- Money Transfers Between Foreign-Owned LLCs (/knowledge/money-transfers-foreign-owned-llcs)

- Form 1040-NR vs Form 1120-F (/knowledge/form-1040-nr-vs-1120-f)

- Form 7004 for Foreign-Owned LLCs (/knowledge/form-7004-foreign-owned-llc)

- Form 5472 Penalty Relief: When Reasonable Cause Works (/knowledge/form-5472-penalty-relief)

- Foreign-Owned LLC Compliance Calendar 2026 (/knowledge/foreign-owned-llc-compliance-calendar)

About the Author

Krishnaveni Raghavan, CPA, EA, is a Certified Public Accountant and IRS-credentialed Enrolled Agent with deep experience in U.S. tax compliance for foreign-owned LLCs, foreign partnerships, multi-entity structures, expats, and cross-border businesses. She leads the international tax practice at Optimize Tax LLC, where she advises on entity classification (Form 8832), Form 5472 and pro forma 1120 filings, Form 8865 (all four categories) including Schedule O, partnership withholding (Forms 8804/8805/8813), Forms 1040-NR and 1120-F, FBAR and Form 8938 reporting, and IRS penalty resolution. As both a CPA and EA, she is licensed to represent taxpayers before the IRS in all 50 states.

Sources & References

- IRS Instructions for Form 8865 — Return of U.S. Persons With Respect to Certain Foreign Partnerships.

- IRS Instructions for Form 5472 — Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business.

- Internal Revenue Code § 6038 — Information reporting with respect to certain foreign corporations and partnerships.

- Internal Revenue Code § 6038A — Information with respect to certain foreign-owned corporations.

- Internal Revenue Code § 6038B — Notice of certain transfers to foreign persons.

- Internal Revenue Code § 6046A — Returns as to interests in foreign partnerships.

- Treasury Regulations § 1.6038-3 — Information returns required of certain United States persons with respect to controlled foreign partnerships.

- Treasury Regulations § 301.7701-3 — Classification of certain business entities (check-the-box).