Table of Contents

ToggleKey Takeaways

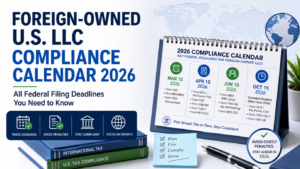

- March 15, 2026: Form 1065 (partnerships), Forms 8804/8805 (Section 1446), partnership Form 7004.

- April 15, 2026: Form 5472 + pro forma 1120 (DEs), Form 1120 (corps), Form 1040-NR (with withholding).

- June 15, 2026: Form 8804 special date if all foreign partners are NRAs; Form 1040-NR (no withholding); Q2 8813.

- Quarterly 8813 deposits: April 15, June 15, September 15, December 15.

- October 15, 2026: Extended Form 5472 + 1120 deadline (after Form 7004).

- Most penalties start at $25,000 (Form 5472) or scale per-partner per-month (Form 1065).

Where This Post Fits

→ What Is Form 5472? (/knowledge/what-is-form-5472)

→ How to File Taxes for a Foreign-Owned Single-Member LLC (2026) (/knowledge/foreign-owned-smllc-tax-filing)

→ Foreign-Owned Multi-Member LLCs: Form 1065 + 8805 (/knowledge/foreign-owned-multi-member-llc-form-1065-8805)

Foreign founders rarely miss a deadline because they didn’t care. They miss it because they had four different deadlines on different schedules, all routed to different IRS addresses.

This calendar consolidates the major federal filing deadlines foreign-owned U.S. LLCs and their owners need to track throughout the year.

Whether you’re operating a foreign-owned single-member LLC, a partnership, or a corporate-elected entity, staying ahead of IRS filing dates can significantly reduce avoidable penalties and compliance issues.

How to Use This Calendar

The quarterly tables below list the federal deadlines most foreign-owned U.S. LLCs encounter, organized by calendar quarter. Three rules govern how to read it:

- Entity type drives which rows apply. A foreign-owned single-member LLC (DE) cares about Form 5472 + pro forma 1120 and the April 15 / October 15 cycle; a multi-member LLC taxed as a partnership cares about Form 1065 + Schedules K-2/K-3 and the March 15 / September 15 cycle plus Section 1446 deposits.

- Routing is not the same as filing. Several of these forms must be paper-filed or faxed to a specific IRS unit — most notably Form 5472 + pro forma 1120 (Ogden, M/S 6112) and the matching Form 7004. Misrouted filings are treated as failures to file.

- Extensions only extend filing, not payment. Estimated tax (including § 1446 deposits via Form 8813) must be paid by the original due date regardless of Form 7004.

Q1 2026 (January–March)

| Date | Form | Who Files |

| January 15, 2026 | Form 8813 (Q4 2025) | Partnerships with foreign partners (§ 1446) |

| January 31, 2026 | Form 1042-S (recipient) | Partnerships paying FDAP to foreign partners |

| Feb 28 / Mar 31, 2026 | Form 1042-S (IRS) | Partnerships paying FDAP |

| March 15, 2026 | Form 1065 + K-1 + K-2/K-3 | MMLLCs taxed as partnerships |

| March 15, 2026 | Form 8804 + Form 8805 | Partnerships (non-NRA-only) |

| March 15, 2026 | Form 7004 (1065 to Sept 15) | Partnerships needing extension |

| March 17, 2026 | Form 1042 annual | Partnerships with FDAP |

Q2 2026 (April–June)

| Date | Form | Who Files |

| April 15, 2026 | Form 5472 + pro forma 1120 | Foreign-owned single-member LLCs (DEs) |

| April 15, 2026 | Form 1120 (regular) | Foreign-owned U.S. corps / corporate-elected LLCs |

| April 15, 2026 | Form 1040-NR (with withholding) | NRA owners with U.S. ECI requiring withholding |

| April 15, 2026 | Form 1120-F (with U.S. office) | Foreign corp with U.S. trade/business + office |

| April 15, 2026 | Form 8813 (Q1) | Partnerships with foreign partners |

| April 15, 2026 | Form 7004 (1120/1120-F/5472 to Oct 15) | Foreign-owned LLCs/corps |

| June 15, 2026 | Form 8813 (Q2) | Partnerships with foreign partners |

| June 15, 2026 | Form 8804 (NRA-only special) | All foreign partners are NRAs |

| June 15, 2026 | Form 1040-NR (no withholding agent) | NRA owners not required to withhold |

| June 15, 2026 | Form 1120-F (no U.S. office) | Foreign corp w/ U.S. trade/business; no U.S. office |

Q3 2026 (July–September)

| Date | Form | Who Files |

| September 15, 2026 | Form 8813 (Q3) | Partnerships with foreign partners |

| September 15, 2026 | Form 1065 (extended) | Partnerships that filed Form 7004 |

| September 15, 2026 | Form 8804 (extended) | Partnerships that filed Form 7004 |

Q4 2026 (October–December)

| Date | Form | Who Files |

| October 15, 2026 | Form 5472 + pro forma 1120 (extended) | Foreign-owned DEs that extended |

| October 15, 2026 | Form 1120/1120-F (extended) | Corps that filed Form 7004 |

| October 15, 2026 | Form 1040-NR (extended) | NRA owners that filed extensions |

| December 15, 2026 | Form 8813 (Q4) | Partnerships with foreign partners |

| Year-round | Form 8822-B (responsible party/address) | Within 60 days of any change |

State-Level Deadlines Vary

| State | Annual Filing | Typical Due Date |

| Delaware | Annual franchise tax + report | June 1, 2026 (LLCs); March 1 (corps) |

| Wyoming | Annual report + license tax | First day of LLC’s anniversary month |

| New Mexico | No annual report (LLCs) | N/A — but periodic reporting may apply |

| Florida | Annual report | May 1, 2026 |

| California | SOI + $800 franchise tax | Anniversary month + April 15 |

| Texas | Public Information Report + Franchise Tax | May 15, 2026 |

While this article focuses primarily on federal filing obligations, state compliance deadlines can trigger separate penalties, late fees, or administrative dissolution risks. Foreign founders should track both federal and state filing calendars together as part of a complete compliance strategy.

BOI / Beneficial Ownership Reporting (FinCEN)

BOI under the Corporate Transparency Act has been subject to ongoing legal/regulatory developments. Confirm current FinCEN guidance directly before relying on any calendar entry. Treat BOI as a separate compliance track.

Because BOI requirements continue evolving, many foreign-owned LLCs now maintain separate compliance checklists specifically for FinCEN reporting alongside IRS filing obligations.

The Procedural Details That Cause the Most Penalties

- Form 5472 + pro forma 1120 cannot be e-filed — mail/fax to dedicated Ogden, UT.

- “Foreign-owned U.S. DE” must be written across the top of Form 1120 and Form 7004.

- Form 7004 for foreign-owned DEs goes to the same Ogden address — not regular Form 7004 mailing address.

- Quarterly 8813 deposits use EFTPS.

- Misrouted filings are treated as failures to file — even if mailed on time.

Many foreign-owned LLC penalties happen because filings were mailed incorrectly, sent to the wrong IRS processing center, or submitted without required supporting forms. Administrative compliance errors can become expensive even when taxes are not owed.

December Year-End Checklist for Foreign-Owned LLCs

Before the calendar rolls over, run this checklist in December. Items missed in December become January and February emergencies:

- Confirm Q4 Form 8813 deposit (December 15) was made via EFTPS if the partnership has any foreign partners with ECI.

- Reconcile all intercompany transfers between related LLCs for the year — each related party requires its own Form 5472 with proper categorization (Part IV, V, or VI).

- Verify the responsible party on file with the IRS is current. File Form 8822-B within 60 days of any change.

- Confirm all foreign partners have valid ITINs or pending W-7 applications for Schedule K-1, K-3, and Form 8805 reporting.

- Pull bank statements for each LLC and tag every transfer with its Form 5472 category before the books close.

- Refresh FinCEN BOI filing status — confirm current FinCEN guidance and any beneficial-ownership changes during the year.

- Calendar the March 15, April 15, and June 15 deadlines now — with the correct IRS routing address noted next to each.

- Decide which entities will need Form 7004 extensions and pre-stage the extension packets with the correct codes (09 partnerships, 12 corps/DEs, 15 1120-F, 08 8804).

Frequently Asked Questions

When is the Form 5472 deadline in 2026?

April 15, 2026 for calendar-year filers. Form 7004 extends to October 15, 2026.

When is Form 1065 due in 2026?

March 15, 2026 for calendar-year partnerships. Form 7004 extends to September 15.

Section 1446 quarterly deposits (Form 8813) 2026?

April 15, June 15, September 15, December 15.

When is the Form 1040-NR deadline?

April 15, 2026 if subject to wage withholding; June 15 otherwise. Form 4868 extends to October 15.

When is Form 8804 due if all foreign partners are NRAs?

June 15, 2026 instead of March 15.

Do foreign-owned LLCs need to file BOI?

BOI requirements have been subject to ongoing developments. Confirm current FinCEN guidance.

Why is a foreign-owned LLC compliance calendar important?

Foreign-owned LLCs often face multiple overlapping IRS filing requirements, including Form 5472, Form 1065, Form 1040-NR, Form 8804/8805, and quarterly withholding deposits. A centralized compliance calendar helps reduce missed deadlines, penalty exposure, and extension filing issues.

The Bottom Line

Compliance is half-knowledge, half-discipline. The forms are not difficult when you know they’re coming.

Using a centralized compliance calendar can help foreign founders stay ahead of federal deadlines, state obligations, extension filings, and international reporting requirements before penalties begin accumulating.

Want This as a Downloadable PDF?

Optimize Tax LLC publishes an annual foreign-owned LLC compliance calendar with state-by-state deadlines, IRS routing rules, and a printable checklist. Schedule at Optimize Tax LLC.

Continue Reading: The Form 5472 Knowledge Series

- What Is Form 5472? A Plain-English Guide for Foreign-Owned LLCs (pillar) (/knowledge/what-is-form-5472)

- Do You Need an EIN for a Foreign-Owned LLC? (/knowledge/ein-foreign-owned-llc)

- Form 8832 Entity Classification Election (/knowledge/form-8832-entity-classification)

- Do I Need to File Form 5472 If My LLC Had No Activity? (/knowledge/form-5472-no-activity)

- How to File Taxes for a Foreign-Owned Single-Member LLC (2026) (/knowledge/foreign-owned-smllc-tax-filing)

- What Is a Form 1120 Pro Forma? (/knowledge/form-1120-pro-forma)

- Do Partnerships Need to File Form 5472? (/knowledge/do-partnerships-file-form-5472)

- Foreign-Owned Multi-Member LLCs: Form 1065 + 8805 (/knowledge/foreign-owned-multi-member-llc-form-1065-8805)

- Schedules K-2 and K-3: International Reporting for Partnerships (/knowledge/schedules-k2-k3-partnerships)

- Money Transfers Between Foreign-Owned LLCs (/knowledge/money-transfers-foreign-owned-llcs)

- Form 1040-NR vs Form 1120-F (/knowledge/form-1040-nr-vs-1120-f)

- Form 8865 vs Form 5472 (/knowledge/form-8865-vs-form-5472)

- Form 7004 for Foreign-Owned LLCs (/knowledge/form-7004-foreign-owned-llc)

- Form 5472 Penalty Relief: When Reasonable Cause Works (/knowledge/form-5472-penalty-relief)

About the Author

Krishnaveni Raghavan, CPA, EA, is a Certified Public Accountant and IRS-credentialed Enrolled Agent with deep experience in U.S. tax compliance for foreign-owned LLCs, multi-entity structures, expats, and cross-border businesses. She leads the international tax practice at Optimize Tax LLC, where she advises on full-year compliance calendars across Form 5472, Form 1065 with Schedules K-2/K-3, Section 1446 withholding (Forms 8804/8805/8813), Forms 1040-NR and 1120-F, Form 7004 extensions, FinCEN BOI reporting, and IRS penalty resolution. As both a CPA and EA, she is licensed to represent taxpayers before the IRS in all 50 states.

Sources & References

- IRS Instructions for Forms 5472, 1120, 1065, 8804, 8805, 8813, 1040-NR, 1120-F, 7004, 1042, 1042-S, and 8822-B.

- IRS Online Tax Calendar for Businesses and Self-Employed (irs.gov/businesses).

- Internal Revenue Code § 6038A — Information with respect to certain foreign-owned corporations.

- Internal Revenue Code § 6072 — Time for filing income tax returns.

- Internal Revenue Code § 6651 — Failure to file tax return or to pay tax.

- Internal Revenue Code § 6655 — Failure by corporation to pay estimated income tax.

- Internal Revenue Code § 1446 — Withholding of tax on foreign partners’ share of effectively connected income.

- Treasury Regulations § 1.6038A-1 — General requirements and definitions.

- Treasury Regulations § 1.1446-3 — Time and manner of calculating and paying over the 1446 tax.

- FinCEN Beneficial Ownership Information (BOI) reporting guidance (fincen.gov).

- State Department of Revenue annual-report and franchise-tax requirements.