Key Takeaways

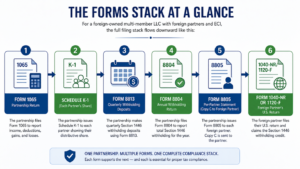

- A foreign-owned multi-member LLC defaults to partnership tax treatment — it files Form 1065, not Form 5472.

- Each partner receives a Schedule K-1 reporting their share of income, deductions, and credits.

- If foreign partners have effectively connected income (ECI), the partnership must withhold under Section 1446 withholding — Forms 8813 (quarterly), 8804 (annual return), and 8805 (per-partner statement).

- Section 1446 withholding rates are tied to the highest applicable tax rate — currently 37% for individual foreign partners, 21% for foreign corporate partners.

- Foreign partners attach Copy C of Form 8805 to their U.S. return (1040-NR or 1120-F) to claim the withholding as a credit.

- The withholding calendar is year-round — not a March 15 event. Quarterly 8813 deposits are due during the tax year.

- Penalties for late or missing 1065 / 8804 / 8805 filings can be substantial and stack across forms.

Where This Post Fits

This is the procedural deep-dive on filing for a foreign-owned multi-member LLC. If you are still trying to figure out which form applies to your structure at all, start here:

→ What Is Form 5472? A Plain-English Guide for Foreign-Owned LLCs

→ Do Partnerships Need to File Form 5472? (/knowledge/do-partnerships-file-form-5472)

→ Schedules K-2 and K-3: International Reporting for Partnerships (/knowledge/schedules-k2-k3-partnerships)

→ Form 7004: How to Extend Without Killing Your Filing (/knowledge/form-7004-foreign-owned-llc)

→ Foreign-Owned LLC Compliance Calendar 2026 (/knowledge/foreign-owned-llc-compliance-calendar)

Two founders set up a U.S. LLC and split ownership 50/50. They assume the tax filing will look like one packet at year-end. Then they realize the IRS does not see one entity — it sees a partnership with foreign partners, and a different filing stack entirely.

Here is the part most foreign founders miss: for a multi-member foreign-owned LLC, the question is not Form 5472. It is a partnership return, partner-level statements, and a year-round withholding calendar that starts long before the filing deadline arrives.

This guide walks through exactly how the filing works in 2026 — in the order the IRS expects you to do it. The discussion below also incorporates practical Form 1065 instructions, Form 8805 instructions, and common Section 1446 withholding compliance issues foreign founders encounter during filing season.

Step 1: Confirm the LLC Is Taxed as a Partnership

A domestic LLC with two or more members defaults to partnership treatment unless it filed Form 8832 to elect corporate tax treatment. If no election was made, the IRS treats it as a partnership for federal tax purposes — which means the filing path runs through Form 1065, not Form 5472.

If your LLC elected corporate treatment, stop here. The analysis changes completely — review the partnerships and Form 5472 guides linked above to see which corporate path applies.

For many foreign founders, this is the single most important classification issue because the entire compliance framework for a foreign-owned MMLLC depends on whether partnership tax treatment still applies.

Step 2: File Form 1065 — the Partnership Return

Form 1065 is the partnership’s annual information return. The IRS uses it to see income, deductions, gains, and losses at the partnership level. The partnership itself does not pay income tax — those items pass through to the partners on Schedule K-1.

Key Form 1065 Instructions for Foreign-Owned Multi-Member LLCs

- Due date: March 15 for calendar-year domestic partnerships (15th day of the 3rd month after year-end).

- Extension: Form 7004 extends the filing to September 15 — but it must be filed by the original due date.

- Schedules K-2 and K-3 are required for partnerships with international items — effectively all foreign-owned multi-member LLCs.

- A late or substantially incomplete Form 1065 carries a per-partner, per-month penalty that compounds quickly.

Form 1065 is not just paperwork. It is the source document the rest of the partnership stack depends on. If the 1065 is late, the partner-level filings unravel with it.

Many founders reviewing IRS Form 1065 instructions focus only on the filing deadline. In practice, the higher-risk issue is filing an incomplete return — especially when international schedules or foreign partner disclosures are omitted.

Step 3: Issue Schedule K-1 to Each Partner

Schedule K-1 reports each partner’s distributive share of the partnership’s income, deductions, credits, and other items. Each partner uses the K-1 to file their own return — and, where applicable, state and local filings.

For a multi-member LLC, the K-1 is where one business splits into multiple tax stories. Each partner’s share matters — especially when foreign partners are involved, because that share drives the next step: withholding.

Step 4: If You Have Foreign Partners, Section 1446 Withholding Is Mandatory

This is where compliance gets serious. When a partnership has foreign partners and effectively connected taxable income (ECI), Section 1446 of the Internal Revenue Code requires the partnership to withhold tax on the foreign partners’ allocable share — even if no actual distribution is made.

The mechanics use three forms:

- Form 8813 — quarterly Section 1446 withholding payment vouchers.

- Form 8804 — annual partnership return reporting the total withholding.

- Form 8805 — per-partner statement showing each foreign partner’s share of ECI and withholding.

Important: Section 1446 withholding rates are tied to the highest applicable rate. For 2026 returns, that is 37% for individual foreign partners (non-resident aliens) and 21% for foreign corporate partners. These rates apply to the partner’s allocable share of ECI — not to net distributions.

Foreign-owned partnerships frequently misunderstand this rule because they assume withholding only applies when money is physically distributed. Under Section 1446 withholding rules, the taxable income allocation itself is what triggers the obligation.

Worked Example: $100,000 of ECI Allocated to a Non-resident Alien Partner

How the Numbers Flow

Facts: A two-member U.S. LLC (taxed as a partnership) has a 50/50 non-resident alien partner. For 2026, the partnership has $200,000 of effectively connected taxable income. The NRA partner’s allocable share is $100,000.

Step 1 — Section 1446 withholding rate: 37% (highest individual rate).

Step 2 — Withholding amount: $100,000 × 37% = $37,000.

Step 3 — Quarterly deposits via Form 8813: roughly $9,250 per quarter.

Step 4 — Annual Form 8804 reports $37,000 total withheld for the partnership.

Step 5 — Form 8805 issued to the NRA partner showing $100,000 ECI and $37,000 withheld; Copy C goes to the partner.

Step 6 — The NRA partner files Form 1040-NR, reports the $100,000 of ECI, and claims the $37,000 as a withholding credit using Copy C of Form 8805.

If actual U.S. tax liability is less than $37,000, the partner files for a refund. If the partnership missed the quarterly deposits, the partnership — not the partner — owes the underpayment interest and penalties.

Step 5: Form 8805 — the Foreign Partner’s Tax-Credit Slip

Form 8805 is the document that connects the partnership’s withholding to the foreign partner’s personal U.S. return. It tells the partner exactly how much ECI was allocated and how much tax was withheld under Section 1446 for the year.

The partnership keeps one copy and files it with Form 8804. A second copy (Copy C) is sent to the foreign partner. The partner attaches Copy C of Form 8805 to their U.S. return — Form 1040-NR for nonresident individuals, Form 1120-F for foreign corporations — to claim the withholding as a credit against their actual U.S. tax liability.

Important Form 8805 Instructions Foreign Partners Should Understand

Without a properly issued 8805, the foreign partner cannot claim the credit. That converts a withheld tax into a lost tax — which is exactly the kind of error that ends partner relationships.

Foreign partners should also confirm that the EIN, withholding amount, and allocable income reported on Form 8805 match the partnership’s Form 8804 filing. Even small mismatches can delay refunds or trigger IRS notices.

Step 6: The Withholding Calendar Is Year-Round, Not a March 15 Event

This is where most foreign-owned partnerships get caught. They treat tax compliance as a year-end exercise. Section 1446 withholding doesn’t work that way. Quarterly 8813 deposits are due during the tax year — not after it.

2026 Withholding & Filing Calendar (Calendar-Year Partnerships)

| Date | Form / Action | Notes | ||

| April 15, 2026 | Form 8813 (Q1) | First quarterly Section 1446 deposit | ||

| June 15, 2026 | Form 8813 (Q2) | Second quarterly deposit | ||

| September 15, 2026 | Form 8813 (Q3) | Third quarterly deposit | ||

| December 15, 2026 | Form 8813 (Q4) | Fourth quarterly deposit | ||

| March 15, 2027 | Form 1065 + K-1s | Partnership return due; K-2/K-3 required | ||

| March 15, 2027 | Form 8804 + 8805 | Annual withholding return + statements | ||

| April 15, 2027 | 1040-NR / 1120-F | Foreign partner returns with 8805 Copy C | ||

| September 15, 2027 | Extended 1065 | If Form 7004 filed by March 15 | ||

| Form | What It Is | 2026 Due Date | ||

| Form 8813 (Q1) | Section 1446 quarterly withholding payment | April 15, 2026 | ||

| Form 8813 (Q2) | Section 1446 quarterly withholding payment | June 15, 2026 | ||

| Form 8813 (Q3) | Section 1446 quarterly withholding payment | September 15, 2026 | ||

| Form 1065 + K-1s + K-2/K-3 | Partnership return + partner statements | March 15, 2026 (for 2025 return); extends to Sept 15, 2026 with Form 7004 | ||

| Form 8813 (Q4) | Section 1446 quarterly withholding payment | December 15, 2026 | ||

| Form 8804 + 8805 | Annual withholding return + per-partner statements | March 15, 2026 (15th day of 3rd month after year-end) | ||

| Form 8804 — if all foreign partners are NRAs | Special extended date applies | June 15, 2026 (15th day of 6th month) | ||

Two practical points buried in that table:

- If the partnership’s non-resident alien partners are its only foreign partners, the IRS allows Form 8804 to be filed by the 15th day of the 6th month after year-end — a useful extension for cleaner compliance, but not automatic.

- Form 1065 and Form 8804 share the same default March 15 due date. They are different forms, filed separately, with different penalty regimes if missed.

The Forms Stack at a Glance

Where DIY Filings Most Often Go Wrong

Across MMLLC engagements, the same mistakes show up:

- Filing Form 5472 instead of Form 1065 — the wrong form entirely.

- Filing Form 1065 but skipping Schedules K-2/K-3, which the IRS treats as substantially incomplete for partnerships with international items.

- Skipping Section 1446 withholding because no actual distributions were made — ECI allocation, not distribution, is the trigger.

- Missing Form 8813 quarterly deposits and waiting until year-end to remit Section 1446 tax — underpayment interest and penalties apply.

- Issuing Schedule K-1 but forgetting Form 8805 Copy C, leaving the foreign partner unable to claim their withholding credit.

- Mixing up the Form 8804 due date for partnerships with all-NRA partners (June 15) versus mixed foreign partners (March 15).

Many of these issues begin with founders relying on generic bookkeeping providers instead of specialized accounting services to small business owners dealing with international tax exposure. Cross-border partnership filings are procedural, deadline-sensitive, and heavily penalty-driven.

When Professional Preparation Is Strongly Recommended

If any of these apply, professional preparation is strongly recommended over DIY:

- Foreign partners with ECI — Section 1446 withholding alone is high-risk, high-penalty territory.

- Tiered partnership structures (partnership owning a partnership).

- FIRPTA exposure on U.S. real property dispositions.

- Mid-year change in partner mix (admission, withdrawal, or transfer of interest).

- Mid-year Form 8832 corporate election.

- Prior-year missed filings or active IRS correspondence.

- Foreign partners receiving guaranteed payments or special allocations.

Founders frequently underestimate how quickly partnership compliance expands once withholding, K-2/K-3 reporting, and foreign partner filings are involved. Experienced accounting services to small business clients with international ownership can often prevent far more expensive cleanup work later.

Frequently Asked Questions

Does a foreign-owned multi-member LLC file Form 5472?

Generally, no. A foreign-owned multi-member LLC defaults to partnership tax treatment and files Form 1065 instead. Form 5472 typically applies to foreign-owned single-member LLCs (disregarded entities) and 25% foreign-owned U.S. corporations.

What is Section 1446 withholding?

Section 1446 withholding requires partnerships with foreign partners to withhold U.S. tax on each foreign partner’s share of effectively connected taxable income (ECI). The current rates are 37% for individual foreign partners and 21% for foreign corporate partners.

Is Section 1446 withholding triggered by distributions or by income allocations?

Income allocations. Even if the partnership makes no distributions, withholding is still required on each foreign partner’s allocable share of ECI.

When is Form 8804 due?

March 15 for calendar-year partnerships (15th day of the 3rd month after year-end). If all foreign partners are nonresident aliens, the deadline shifts to June 15 (15th day of the 6th month).

What are the most important Form 1065 instructions foreign-owned partnerships should know?

The most important Form 1065 instructions involve timely filing, issuing accurate Schedule K-1s, including required K-2/K-3 international schedules, and coordinating the partnership return with Section 1446 withholding filings. Missing international schedules can cause the IRS to treat the filing as substantially incomplete.

What are the most important Form 8805 instructions for foreign partners?

Foreign partners should verify that Form 8805 accurately reflects their allocable share of ECI and withholding. Copy C of Form 8805 must generally be attached to Form 1040-NR or Form 1120-F to properly claim the withholding credit.

How does a foreign partner claim back the Section 1446 withholding?

By filing a U.S. return — Form 1040-NR for nonresident individuals or Form 1120-F for foreign corporations — and attaching Copy C of Form 8805 to claim the withholding as a credit. If actual tax owed is less than the amount withheld, the partner can claim a refund.

What if our partnership missed a quarterly Form 8813 payment?

Underpayment interest and penalties apply at the partnership level. Catch-up deposits should be made as soon as possible, and a reasonable-cause statement may reduce penalties — but acting before the IRS issues a notice strengthens the position significantly.

Can a foreign-owned multi-member LLC e-file?

Form 1065 generally can be e-filed. Forms 8804, 8805, and 8813 have specific filing rules and addresses that should be confirmed for your tax year. Misrouted withholding filings are treated as not filed for penalty purposes.

The Bottom Line

A foreign-owned multi-member LLC files taxes as a partnership first and an international withholding case second. Form 1065 tells the partnership story. Schedule K-1 hands each partner their share. Form 8805 hands the foreign partner the credit slip the IRS expects them to carry into their own return. And Forms 8813 and 8804 keep the withholding clock honest all year long.

The mistake is treating any one of those forms as the whole compliance story. They only work as a stack.

For foreign founders, understanding the relationship between Form 1065 instructions, Form 8805 instructions, and Section 1446 withholding requirements is what separates clean compliance from expensive IRS notices and partner-level filing problems.

Need Help With Your 2026 Partnership Filing?

Optimize Tax LLC works with foreign-owned multi-member LLCs every filing season — Form 1065 with K-2/K-3, Section 1446 withholding quarterly deposits, Forms 8804/8805, and the foreign partners’ 1040-NR or 1120-F returns.

If your LLC has foreign partners and you want a credentialed CPA and EA to manage the full stack, schedule a consultation at Optimize Tax.

Continue Reading: The Form 5472 Knowledge Series

- What Is Form 5472? A Plain-English Guide for Foreign-Owned LLCs (pillar) (/knowledge/what-is-form-5472)

- Do Partnerships Need to File Form 5472? (/knowledge/do-partnerships-file-form-5472) — the entity classification overview that explains why this post exists.

- Do I Need to File Form 5472 If My LLC Had No Activity? (/knowledge/form-5472-no-activity) — the deep dive for single-member LLCs.

- How to File Taxes for a Foreign-Owned Single-Member LLC (2026 Step-by-Step) (/knowledge/foreign-owned-smllc-tax-filing) — single-member procedural walkthrough.

About the Author

Krishnaveni Raghavan, CPA, EA, is a Certified Public Accountant and IRS-credentialed Enrolled Agent with deep experience in U.S. tax compliance for foreign-owned LLCs, partnerships with foreign partners, expats, and cross-border businesses. She leads the international tax practice at Optimize Tax LLC, where she advises on entity classification (Form 8832), Form 1065 with K-2/K-3, Section 1446 withholding (Forms 8804/8805/8813), Form 5472 and pro forma 1120 filings, Forms 1040-NR and 1120-F, and IRS penalty resolution. As both a CPA and EA, she is licensed to represent taxpayers before the IRS in all 50 states.

Sources & References

- IRS Instructions for Form 1065 — U.S. Return of Partnership Income.

- IRS Instructions for Schedules K-2 and K-3 (Form 1065) — Partners’ Distributive Share Items — International.

- IRS Instructions for Form 8804 — Annual Return for Partnership Withholding Tax (Section 1446).

- IRS Instructions for Form 8805 — Foreign Partner’s Information Statement of Section 1446 Withholding Tax.

- IRS Instructions for Form 8813 — Partnership Withholding Tax Payment Voucher (Section 1446).

- IRS Instructions for Form 1040-NR — U.S. Nonresident Alien Income Tax Return.

- IRS Instructions for Form 1120-F — U.S. Income Tax Return of a Foreign Corporation.

- IRS Instructions for Form 8832 — Entity Classification Election.

- IRS Instructions for Form 7004 — Application for Automatic Extension of Time to File Certain Business Income Tax, Information, and Other Returns.

- Internal Revenue Code § 1446 — Withholding tax on foreign partners’ share of effectively connected income.

- Treasury Regulations § 301.7701-3 — Classification of certain business entities (“check-the-box” rules).

- IRS Publication 541 — Partnerships.