Foreign-owned single-member LLC tax filing rules confuse many international founders because the LLC is often treated differently for income tax purposes and IRS information-reporting purposes. In most cases, a foreign-owned U.S. single-member LLC must file Form 5472 with a pro forma Form 1120 — even if the business had little activity or no income.

Missing this filing can trigger an automatic $25,000 IRS penalty.

This step-by-step 2026 guide explains:

- When Form 5472 is required

- How foreign-owned LLC reporting and taxes work

- Whether Form 1040-NR or Form 1120-F also applies

- 2026 filing deadlines and extension rules

- Common mistakes that trigger IRS penalties

- What foreign founders should prepare before filing

Key Takeaways

- A foreign-owned U.S. single-member LLC is disregarded for income tax — but treated as a corporation for Form 5472 reporting under IRC § 6038A.

- Most filings require a pro forma Form 1120 with Form 5472 attached, not a full corporate return.

- Reportable transactions” include capital contributions, distributions, reimbursements, and formation activity — not just sales.

- The 2026 deadline for calendar-year filers is April 15, 2026; Form 7004 extends it to October 15, 2026.

- The penalty for missing or filing an incomplete Form 5472 is $25,000 — plus another $25,000 every 30 days after IRS notice.

- Form 5472 cannot be e-filed for foreign-owned disregarded entities. It must be mailed or faxed to a dedicated IRS address in Ogden, Utah.

- The form is entity-level reporting only — the foreign owner may also need a separate Form 1040-NR or 1120-F.

Does a Foreign-Owned Single-Member LLC Need to File Taxes?

Yes — in many cases, a foreign-owned U.S. single-member LLC must file Form 5472 and a pro forma Form 1120 even if the LLC had no income and no U.S. customers.

The filing obligation is usually triggered by reportable transactions between the foreign owner and the LLC, including:

- Initial funding

- Capital contributions

- Owner reimbursements

- Withdrawals

- Formation expenses paid personally

If the foreign owner is engaged in a U.S. trade or business or earns effectively connected income (ECI), the owner may also need to file:

- Form 1040-NR (for nonresident individuals)

- Form 1120-F (for foreign corporations)

That distinction is one of the most misunderstood parts of foreign owned single member llc tax compliance.

The trap is not forming the LLC. The trap is believing the tax side will be simple because the company has one owner, one bank account, and not much drama.

Here is the part most foreign founders learn the hard way: an LLC that looks dormant under state law can still trigger a federal information-return filing with a $25,000 penalty attached. This guide walks through exactly what a 2026 filing looks like for a foreign-owned U.S. single-member LLC — in the order you should actually do it.

Understanding How the IRS Classifies a Foreign-Owned Single-Member LLC

First: Decide Which Version of Your LLC the IRS Is Looking At

Here is the split that matters most in foreign owned single member llc tax. By default, a single-member LLC is disregarded for federal income tax purposes unless it files Form 8832 and elects to be taxed as a corporation. If it does make that election, the filing path changes materially. This guide covers the most common 2026 setup: a foreign-owned U.S. single-member LLC that stayed in its default disregarded status.

That default status misleads people. A foreign-owned U.S. disregarded entity is still treated as a corporation for the limited purpose of the Section 6038A reporting rules — which is why the IRS can require Form 5472 even though the LLC is otherwise disregarded for income tax.

Read that twice: your LLC can be invisible for income tax purposes and visible for information-reporting purposes in the same tax year. Most mistakes happen because owners understand the LLC under state law, but not the reporting logic the IRS layers on top of it.

Important IRS Classification Rule for Foreign-Owned LLCs

For federal tax purposes, the IRS applies two separate frameworks:

- Entity classification rules

- Information-reporting rules

That is why many foreign founders mistakenly assume that “disregarded entity” means “no filing requirement.” It does not.

A foreign-owned disregarded entity can still have mandatory IRS reporting obligations under IRC § 6038A and Treasury Regulation § 1.6038A-1.

Step 1: Get the Entity Basics Clean Before You Touch a Tax Form

Start with the obvious but often-skipped admin layer: confirm the LLC has been validly formed with the state and has its EIN. The IRS issues EINs at no cost, and businesses generally need one to manage tax filings and reporting. If the principal place of business is outside the U.S., the EIN application has to be done by phone, fax, or mail — not through the IRS online tool.

This sounds basic. It isn’t. If the setup is messy, the filing usually gets messy with it. Good accounting services to small business owners are most valuable here — before year-end — because they keep entity records, owner transactions, and filing identity aligned before the forms start multiplying.

Pre-Filing Setup Checklist

- LLC formation documents on file with the state of formation.

- Active registered agent in the state of formation.

- EIN issued by the IRS (CP 575 or 147C confirmation letter on hand).

- Foreign owner’s ITIN obtained if required for the owner’s personal U.S. filing.

- Separate U.S. business bank account in the LLC’s name.

- Clean ledger of every transfer between the owner and the LLC during the year.

Recommended Recordkeeping for Foreign-Owned LLC Compliance

To reduce IRS filing risk and improve audit readiness, maintain:

- Monthly bookkeeping records

- Copies of all owner contributions and withdrawals

- Bank statements

- Invoices and receipts

- Prior-year IRS filings

- EIN confirmation notices

- Signed operating agreements

- Any intercompany agreements with related entities

Strong documentation matters because Form 5472 Filing Requirements focus heavily on related-party transactions.

Step 2: Figure out Whether Your “Inactive” Year Was Actually Reportable

This is where foreign-owned llc reporting and taxes stop being intuitive. Form 5472 is generally required when a reporting corporation has a reportable transaction with a foreign or domestic related party. For a foreign-owned U.S. disregarded entity, reportable transactions are broader than most founders expect. The IRS instructions specifically include amounts paid or received in connection with formation, dissolution, acquisition, and disposition of the entity, including contributions to and distributions from the entity.

Here is where most people get it wrong: they think no customers means no filing. It does not. If you funded the LLC, reimbursed yourself, paid a company bill personally, or moved money back out, you may already have the kind of related-party activity that turns a quiet year into a Form 5472 year.

There is one narrow escape hatch. The IRS says a reporting corporation is not required to file Form 5472 if it had no reportable transactions of the kinds listed in Parts IV and VI — and, for a foreign-owned U.S. disregarded entity, none of the Part V transactions either. That exception is real, but it is narrower than the word “inactive” suggests.

Common Reportable Transactions That Trigger Form 5472

Many foreign-owned LLCs accidentally trigger filing requirements through ordinary startup activity.

Examples include:

- Funding the LLC during formation

- Paying LLC expenses personally

- Reimbursing the owner

- Transferring intellectual property into the LLC

- Loaning money to the business

- Taking owner distributions

- Payments between affiliated companies under common ownership

Even low-activity LLCs often meet Form 5472 Filing Requirements because the IRS definition of “reportable transaction” is broader than many founders expect.

Step 3: Prepare Form 5472 Like a Transaction Report, Not a Tax Return

Form 5472 is not where you figure your income tax. It is where you disclose the relationship and the movements between the LLC and related parties. The form is used to report transactions that occurred during the tax year of the reporting corporation. If you had reportable transactions with more than one related party, the IRS requires a separate Form 5472 for each one.

That changes how you should gather records. You are not just looking for revenue and expenses. You are looking for:

- Owner funding into the LLC (capital contributions, loans).

- Owner withdrawals (distributions, loan repayments).

- Reimbursements in either direction.

- Intercompany charges with affiliated entities controlled by the same owner.

- Anything else that crossed the line between the LLC and a related party.

This is exactly why founders who wait until tax season end up reconstructing the year from screenshots instead of books.

What the IRS Looks for on Form 5472

The IRS uses Form 5472 primarily as an international information-reporting tool.

The form helps the IRS track:

- Foreign ownership

- Related-party transactions

- Capital movement

- Intercompany activity

- Potential transfer-pricing concerns

- U.S. trade or business indicators

That is why accurate bookkeeping and transaction classification matter long before filing season begins.

Step 4: Attach It to a Pro Forma Form 1120, Not a Full Corporate Return

This is the procedural point that trips up a lot of foreign owners. The IRS says a foreign-owned U.S. disregarded entity must file Form 5472 attached to a pro forma Form 1120 by the due date — even though the entity itself does not otherwise have a regular U.S. corporate income tax return filing requirement.

The only information generally required on that pro forma Form 1120 is the name and address of the foreign-owned disregarded entity and items B and E on the first page. “Foreign-owned U.S. DE” must be written across the top of the Form 1120.

Another detail matters here: the entity uses the same tax year used by its owner for U.S. tax filing requirements, or the calendar year if the owner has no U.S. filing year to anchor to. That sounds like a footnote, but it controls the deadline.

Pro Forma Form 1120 Filing Rules Foreign Owners Often Miss

For foreign-owned disregarded entities:

- The Form 1120 is generally informational only

- It accompanies Form 5472

- It is not usually a full corporate income-tax filing

- “Foreign-owned U.S. DE” must appear clearly at the top

- Incorrect formatting or incomplete information can trigger penalties

This procedural requirement is one reason foreign-owned LLC reporting and taxes become complicated even when the LLC itself has minimal activity.

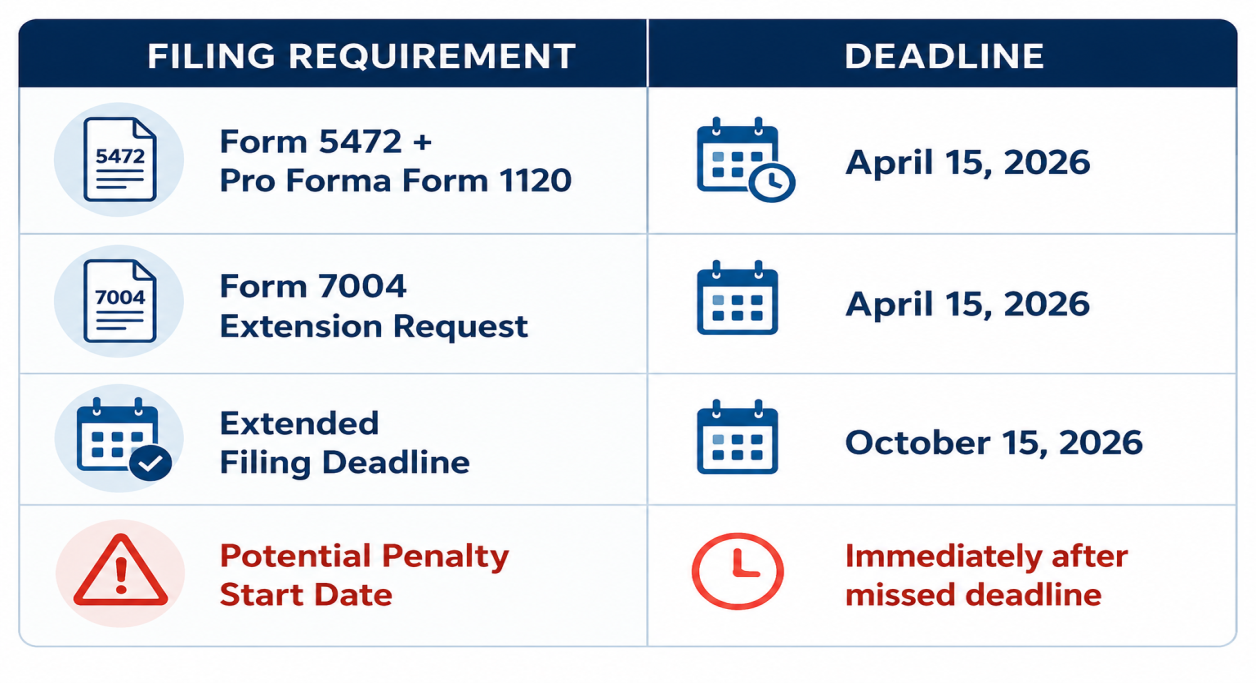

Step 5: Know the 2026 Deadline Before It Becomes a Penalty Story

For this filing path, the due date follows the due date of Form 1120, which is generally the 15th day of the fourth month after the end of the tax year. For a calendar-year filer, that means April 15, 2026.

If you need more time, the IRS allows an extension through Form 7004 — but it must be filed by the regular due date, and for a foreign-owned U.S. disregarded entity it must be faxed or mailed using the special routing instructions, not the regular Form 7004 filing address.

2026 Foreign-Owned LLC Tax Filing Deadlines

| Filing | Original Deadline | Extended Deadline | Where to File |

| Form 5472 + Pro Forma 1120 (Foreign-owned DE) | April 15, 2026 | October 15, 2026 (via Form 7004) | IRS, Ogden UT (mail or fax only) |

| Form 1040-NR (Nonresident individual owner) | April 15, 2026 | October 15, 2026 (via Form 4868) | E-file or mail |

| Form 1120-F (Foreign corporate owner) | April 15, 2026 | October 15, 2026 (via Form 7004) | E-file or mail |

| Form 7004 Extension Request | April 15, 2026 | N/A – must file by original date | IRS, Ogden UT |

| State Annual Reports (varies by state) | Varies by state | Varies by state | State filing office |

Penalty Math — Why Missing This Deadline Is Expensive

- $25,000 base penalty for failure to file or for filing a substantially incomplete Form 5472.

- Additional $25,000 for every 30-day period the failure continues after 90 days from IRS notice.

- No statutory cap. Penalties keep compounding.

- One Form 5472 per related party — multiple related parties means multiple penalties.

Real-world example: a missed 2023 filing, IRS notice in March 2026, return filed September 2026 = $25,000 base + (3 × $25,000) continuing penalty = $100,000 total.

The truth is, missing the form is expensive not because the return is long, but because the IRS treats the obligation seriously. The Form 5472 instructions explicitly state that a substantially incomplete form is treated as a failure to file.

Why the IRS Penalizes Incomplete Form 5472 Filings

The IRS treats:

- Missing forms

- Incorrect routing

- Incomplete disclosures

- Missing related-party information

- Incorrect entity classification reporting

as compliance failures.

For foreign-owned LLCs, procedural mistakes can create the same penalty exposure as failing to file entirely.

Get Your Free Compliance Calendar at optimizetax.io/compliance-calendar/

Get free deadline reminders 30 days in advance with our Compliance Calendar – built specifically for foreign-owned U.S. LLCs.

The penalties above are real – and they are triggered by missing dates, not by making mistakes on the form itself. The simplest protection is knowing your deadlines before they arrive.

Never Miss These Deadlines

Step 6: Do Not Try to E-File the Part You Are Not Allowed to E-File

This is one of those details that sounds too small to matter — until it does. The IRS instructions say foreign-owned U.S. disregarded entities cannot file Form 5472 electronically. Instead, the package must be faxed or mailed to the dedicated IRS address in Ogden, Utah, and “Foreign-owned U.S. DE” should be written across the top of the Form 1120.

That is why generic software advice can be risky here. The form itself is not conceptually impossible. The routing rules are what catch people. A return rejected because it was e-filed when it should have been mailed is treated, for penalty purposes, as if it were never filed at all.

Mailing and Routing Rules Matter

Foreign-owned LLC compliance problems are often procedural rather than technical.

Common issues include:

- Mailing the package to the wrong IRS address

- Using software that improperly e-files Form 5472

- Forgetting required labeling language

- Missing signatures

- Sending incomplete attachment packages

For international founders, these small procedural errors often become expensive IRS notices months later.

Step 7: Check Whether the Owner Has a Separate U.S. Return Too

This is where a lot of articles oversimplify the story. Form 5472 is entity-level information reporting. It does not always settle the owner’s own U.S. tax filing position.

If a foreign person is engaged in a U.S. trade or business, the IRS treats income connected with that business as effectively connected income (ECI). For a nonresident alien, that income is generally reported on Form 1040-NR. If the owner is a foreign corporation, Form 1120-F is the return used to report its U.S. income tax liability.

Quick Reference: Which Owner-Level Return May Apply

| Owner Type | U.S. Activity | Likely Owner-Level Return |

| Nonresident individual | No U.S. trade or business; no ECI | No 1040-NR required (Form 5472 only) |

| Nonresident individual | U.S. trade or business or ECI | Form 1040-NR + Form 5472 package |

| Foreign corporation | U.S. trade or business or ECI | Form 1120-F + Form 5472 package |

That is the part people miss when they reduce the topic to Form 5472 Filing Requirements alone. The form may be mandatory even in a low-activity year, but a real tax filing can also sit behind it if the facts rise to a U.S. trade or business or create taxable U.S. income for the owner. This is where an experienced accounting services to small business team stops being optional and starts saving you from filing one piece correctly while missing the rest.

When Foreign Owners Usually Need Form 1040-NR or Form 1120-F

Additional owner-level tax filings are commonly triggered by:

- U.S.-source income

- Effectively connected income (ECI)

- Employees or contractors operating in the U.S.

- U.S.-based inventory or fulfillment

- Dependent-agent activities

- Certain service-based business operations

Determining whether ECI exists requires factual analysis and should not be guessed based on internet summaries alone.

Where DIY Filings Most Often Go Wrong

Across foreign-owned LLC engagements, the same handful of mistakes show up repeatedly when founders self-prepare:

- E-filing the package even though the IRS does not accept e-filed Form 5472 for foreign-owned DEs.

- Mailing the return to the standard Form 1120 address instead of the dedicated Ogden address.

- Forgetting to write “Foreign-owned U.S. DE” across the top of Form 1120 (and Form 7004 if extended).

- Treating capital contributions at formation as “not reportable” — they are.

- Filing one Form 5472 when there are multiple related parties (each requires its own form).

- Filing the LLC’s 5472 but missing the owner’s separate Form 1040-NR or 1120-F when ECI exists.

- Trying to extend the 2026 deadline using Form 7004 sent to the wrong address — a misrouted extension is no extension at all.

Additional Foreign-Owned LLC Tax Mistakes to Avoid

Other frequent compliance problems include:

- Mixing personal and business expenses

- Operating without bookkeeping records

- Using nominee structures incorrectly

- Ignoring state-level franchise taxes

- Missing final-year filing obligations after dissolution

- Assuming “no income” means “no filing requirement”

Many foreign founders only discover these issues after receiving an IRS penalty notice.

When Professional Preparation Is Strongly Recommended

If any of these apply to your LLC, professional preparation is strongly recommended over DIY:

- Multiple foreign related parties (multiple Form 5472s required).

- Multi-year catch-up filings or prior-year returns never filed.

- You have already received an IRS notice or penalty assessment.

- Non-cash transactions (services performed, property used, below-market transfers).

- Mid-year ownership change, restructuring, or entity classification election.

- Dissolution year or final-return filing.

- The owner has effectively connected U.S. income (ECI) requiring Form 1040-NR or 1120-F.

Why International Founders Use Specialized Tax Professionals

Foreign-owned LLC compliance crosses:

- International tax rules

- IRS information reporting

- Entity classification regulations

- State filing obligations

- Cross-border transaction analysis

Working with a CPA or EA experienced in foreign-owned LLC reporting and taxes can reduce penalty exposure and help ensure both entity-level and owner-level filings are handled correctly.

Frequently Asked Questions

[DEV NOTE: Add FAQPage JSON-LD schema with @type FAQPage containing all 9 Q&A pairs as mainEntity array. Match format in pillar page final_form_5472_conversational_cpa.html lines 60-96.]

Do I have to file U.S. taxes if my single-member LLC had no income?

Possibly yes — but as an information return, not an income tax return. If the LLC had any reportable transaction with its foreign owner (including formation funding), Form 5472 attached to a pro forma Form 1120 is generally required.

What if I never opened a U.S. bank account or did anything with the LLC?

If there were truly no reportable transactions — no contributions, no distributions, no payments in either direction — the no-reportable-transaction exception may apply. The standard is strict, so confirm before assuming.

Can I file Form 5472 by myself?

Technically yes. In practice, the procedural rules (mailing-only filing, dedicated IRS address, label requirements, separate forms per related party) catch most DIY filers. The penalty for getting it wrong is $25,000.

What is the 2026 filing deadline?

April 15, 2026, for calendar-year filers. Form 7004 extends it to October 15, 2026 — but only if filed by the original due date and routed to the special IRS address.

Do I also have to file a Form 1040-NR?

Only if you, as the foreign owner, have effectively connected U.S. income or other U.S.-source income that requires it. A foreign corporate owner with ECI files Form 1120-F instead.

What happens if I missed prior years?

Catch-up filings are possible, and reasonable-cause penalty relief is sometimes available — but the position is much stronger when you file before the IRS contacts you. Once a notice is issued, the leverage shifts.

Does my state require a separate filing too?

Often yes. Most states require an annual report or franchise-tax filing for the LLC, separate from federal Form 5472. Delaware, California, Wyoming, and New Mexico each have their own rules and fees.

Can a foreign-owned LLC have no tax return but still have a filing requirement?

Yes. That is one of the most misunderstood aspects of foreign owned single member llc tax compliance. A disregarded entity may have no federal income-tax return requirement while still having mandatory Form 5472 information-reporting obligations.

Is Form 5472 required for LLC formation funding?

Usually yes. Initial capital contributions and other owner funding transactions are commonly treated as reportable transactions under IRS rules.

The Part Worth Remembering

A foreign-owned single-member LLC is easy to form because the state only asks whether the entity exists. The IRS asks a harder question:

What moved, who owned it, and did you write it down when you were supposed to?

That is the test the IRS applies on top of the LLC — and it is the test most founders are not prepared for in their first filing year. The fix is not complicated. It just has to be on time, in the right form, sent to the right address, signed by the right person, and supported by records you started keeping months before the deadline.

Need Help With Your 2026 Filing?

Optimize Tax LLC works with foreign founders of U.S. single-member LLCs every filing season — from first-year compliance to multi-year catch-up filings, penalty-relief letters, and owner-level 1040-NR or 1120-F returns.

Services commonly include:

- Form 5472 preparation

- Pro forma Form 1120 filings

- IRS penalty-response assistance

- Form 1040-NR preparation

- Form 1120-F preparation

- International bookkeeping support

- Multi-year compliance cleanup

- Reasonable-cause penalty relief requests

If you want a credentialed CPA and EA to prepare and sign your 2026 filing, schedule a consultation at optimizetax.io.

Related Reading

- Form 5472 Filing Guide for Foreign-Owned LLCs

- Do I Need to File Form 5472 If My LLC Had No Activity?

- How to apply for an EIN for a Foreign-Owned LLC

- Form 8832 Entity Classification

- Pro Forma Form 1120: What Foreign Owners Actually Need to Complete

- Form 7004: How Foreign-Owned LLCs Request a Filing Extension

About the Author

Krishnaveni Raghavan, CPA, EA, is a Certified Public Accountant and IRS-credentialed Enrolled Agent with deep experience in U.S. tax compliance for foreign-owned LLCs, expats, and cross-border businesses. She leads the international tax practice at Optimize Tax LLC, where she advises foreign founders on entity structuring, Form 5472 and pro forma 1120 filings, partnership withholding (Forms 8804/8805), Forms 1040-NR and 1120-F, and IRS penalty resolution. As both a CPA and EA, she is licensed to represent taxpayers before the IRS in all 50 states.

Why This Guide Can Be Trusted

This article was prepared and reviewed by a licensed CPA and IRS-authorized Enrolled Agent experienced in international tax compliance and foreign-owned LLC reporting.

The guidance is based on:

- Current IRS instructions

- Treasury Regulations

- IRC §§ 6038A and 6038C

- Actual filing patterns seen in foreign-owned LLC compliance engagements

The article is updated for the 2026 filing season and designed specifically for foreign founders navigating U.S. LLC compliance requirements.

Sources & References

- IRS Instructions for Form 5472 — Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business.

- IRS Instructions for Form 1120 — U.S. Corporation Income Tax Return (used as pro forma for foreign-owned DEs).

- IRS Instructions for Form 7004 — Application for Automatic Extension of Time to File Certain Business Income Tax, Information, and Other Returns.

- IRS Instructions for Form 1040-NR — U.S. Nonresident Alien Income Tax Return.

- IRS Instructions for Form 1120-F — U.S. Income Tax Return of a Foreign Corporation.

- Form 8832 — Entity Classification Election.

- Internal Revenue Code §§ 6038A and 6038C — Information requirements for foreign-owned and foreign corporations.

- Treasury Regulations § 1.6038A-1 — General requirements (including 2017 extension to foreign-owned U.S. disregarded entities).

- IRS Publication on EIN — How to Apply for an Employer Identification Number (international applicants).