Most foreign-owned LLCs need an EIN for IRS reporting, banking, payroll, and tax compliance. International applicants usually cannot use the IRS online EIN system and must apply through Form SS-4 by phone, fax, or mail.

Key Takeaways

- Most foreign-owned U.S. LLCs need an EIN — especially if they will file Form 5472, hire employees, owe excise tax, or open a U.S. bank account.

- The IRS online EIN tool is unavailable to applicants whose principal place of business is outside the U.S. International applicants must use Form SS-4 by phone, fax, or mail.

- The phone line for international EIN applicants is 267-941-1099 (Mon–Fri); the IRS may then request a signed SS-4 by fax or mail within 24 hours.

- The responsible party on the EIN application must be a real person who controls the entity — not a formation agent or nominee.

- If the responsible party has no SSN or ITIN, line 7b of Form SS-4 can show “foreign” — but a value must be entered; it cannot be left blank.

- Any change to the responsible party, address, or location must be reported on Form 8822-B — within 60 days for responsible-party changes.

Where This Post Fits

The EIN is the first piece of compliance infrastructure for any U.S. LLC — it shows up before Form 5472, before Form 1065, and before any owner-level return. If you’re looking for what comes next:

→ foreign-owned LLC Form 5472 filing guide

→ foreign-owned single-member LLC tax filing guide (2026 Step-by-Step)

→ Form 1065 filing rules for foreign-owned multi-member LLCs

A foreign founder can form an LLC in a day and still get stuck for weeks on one deceptively small question: does this company need its own IRS number, or can the owner move forward without it?

The truth is, an EIN is often treated like a minor setup step — right up until it becomes the thing blocking tax filings, payroll, banking, or the first real compliance deadline.

The Short Answer: Yes, More Often Than People Expect

If you are asking whether a foreign-owned LLC needs an EIN, the safest answer is usually yes — especially if the entity will file tax forms, hire employees, handle certain excise taxes, or operate as a foreign-owned U.S. disregarded entity that must file Form 5472.

The IRS says Form SS-4 is used to obtain an EIN for tax filing and reporting purposes, and its single-member LLC guidance says most new single-member disregarded LLCs will need one. The SS-4 instructions go further: a foreign-owned U.S. disregarded entity applying because it must file Form 5472 should identify that exact reason on the application.

Where most people get it wrong: they hear that a single-member LLC is “disregarded” and assume the federal paperwork is basically optional. It isn’t. For income tax classification, a one-owner LLC may be disregarded by default, but the IRS still requires an EIN in several common situations — and foreign-owned disregarded entities land in a more sensitive reporting category than many founders realize.

When the IRS Clearly Expects You to Have an EIN

There are a few moments when the question is barely a question at all:

- The LLC has employees or owes excise tax — the IRS says the LLC must use its own EIN.

- The LLC is a foreign-owned U.S. disregarded entity that must file Form 5472 — the SS-4 instructions explicitly walk through how to request the EIN and what description to use.

- The LLC needs an EIN for banking purposes — the IRS lists “banking purpose” as a specific reason for requesting an EIN, even when no tax filing requirement exists yet.

- The LLC will file partnership returns (Form 1065) — a multi-member LLC needs its own EIN to file.

- The LLC plans to elect corporate tax treatment via Form 8832 — corporate filings require an EIN.

These are some of the most common situations where founders apply for EIN LLC filings shortly after formation. In practice, foreign-owned LLC reporting and taxes often begin earlier than many international founders expect.

That last group is easy to miss. It is tempting to think an EIN exists only for tax returns. The IRS does not frame it that narrowly. It treats the EIN as the business’s tax identifier and allows applicants to request one for banking purposes alone. So when founders ask whether to apply for EIN LLC paperwork early or wait until tax season, the IRS materials lean toward early clarity, not improvisation later.

How to Apply for an EIN for an LLC Outside the U.S.

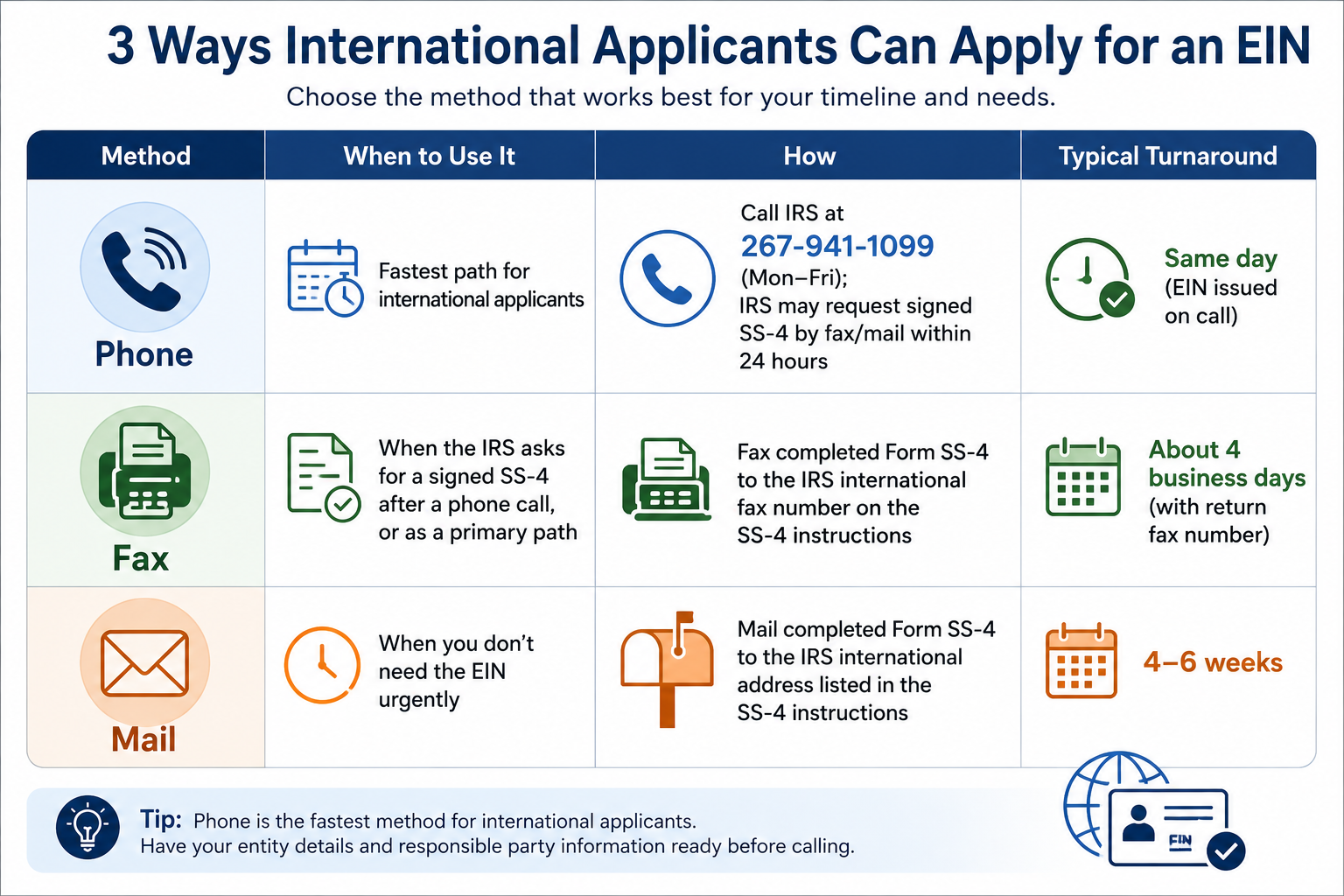

International founders searching how to apply for EIN LLC paperwork often discover that the IRS process is different for foreign applicants. Most non-U.S. founders must request EIN for a foreign owned LLC using Form SS-4 by phone, fax, or mail instead of the regular online EIN system.

Can Foreign Owners Apply for an EIN Online?

No. International applicants generally cannot use the IRS online EIN application system if the principal place of business is outside the United States.

Instead, foreign founders usually apply using:

- Form SS-4 by phone

- fax

- or mail

The Gray Area Foreign Owners Should Be Cautious About

Not every LLC automatically needs a brand-new EIN in every scenario. The IRS page on when to get a new EIN says a single-member LLC may not need a new EIN if it reports income tax as a branch or division of another entity and has no employees or excise tax. It also says a sole proprietor may use their existing sole-proprietor EIN for a new single-member LLC in limited circumstances — if the LLC does not elect corporate tax treatment and has no employees or excise tax obligations.

Here is the practical problem for foreign owners: those exceptions do not erase the foreign-owned disregarded entity rules. If the LLC is in the Form 5472 lane, the SS-4 instructions specifically contemplate an EIN request for that reason. Foreign-owned single-member LLCs should be very cautious about reading general domestic exceptions too broadly — the safer path is to apply for the EIN.

How to Apply When You Are Outside the United States

This is the part that surprises people the first time they try it. The IRS online EIN tool is only available when the principal place of business is in the U.S. or U.S. territories, the responsible party is in control of the entity, and the filer has the responsible party’s SSN or ITIN. If the principal place of business is outside the U.S., the IRS says you cannot use the online application. Instead, you apply by phone, fax, or mail.

EIN Application Paths for International Applicants

| Method | How It Works | Timeline | Est. Cost (DIY) | Risk Level |

| Phone (267-941-1099) | Call IRS intl line; fax signed SS-4 within 24 hrs | Same day | Free | Low |

| Fax | Fax completed SS-4 with return fax number | ~4 business days | Free | Low |

| Mail SS-4 to IRS campus | 4-6 weeks | Free | Medium – no tracking | |

| Third-Party Service | Formation agent files for you | 1-5 business days | \-\+ | Higher – RP errors common |

This is also where founders searching how to apply for EIN LLC or request EIN for a foreign owned LLC run into conflicting online advice. The official IRS answer is cleaner than many blog posts: international applicants don’t use the regular online system, and they should use Form SS-4 by phone, fax, or mail under the IRS’s current international instructions.

Responsible Party Rules for Foreign-Owned LLCs

The Responsible Party Rule Matters More Than Founders Expect

The IRS says the responsible party on the EIN application must be an actual person, not another entity, unless the applicant is a government entity. Its responsible-party guidance describes that person as the one who ultimately owns or controls the entity, or exercises effective control over its funds and assets.

That detail matters for foreign-owned LLCs because nominee services and formation agents cannot simply step in as the real responsible party. If a formation agent fills in their own information to speed up the application, the IRS record reflects the wrong person — and that mismatch creates problems later when the LLC needs to file, change addresses, or update ownership.

Caution: Third-Party Designee Risks

When you check the Third-Party Designee box on Form SS-4, you authorize that person to receive your EIN and discuss the application with the IRS. Some formation services use this access without clearly explaining the scope. Risks include: (1) the designee receiving sensitive IRS correspondence meant for you, (2) unauthorized changes to your entity records, and (3) difficulty reclaiming control if the relationship ends. If you use a third party, choose a credentialed professional (CPA/EA) bound by ethical standards – not an anonymous online service with no fiduciary obligation.

The Practical Relief Valve on Line 7b

The SS-4 instructions say that on line 7b, if the responsible party does not have and is ineligible to obtain an SSN or ITIN, you may enter “foreign” (or N/A in some applications) — but a value must be entered; it cannot be left blank.

This rule is easy to overlook and incredibly useful for international founders who do not yet have a U.S. taxpayer ID. It is what allows a non-U.S. person to obtain an EIN without first obtaining an ITIN.

Why This Tiny Number Creates Outsized Problems Later

An EIN is not glamorous. It is administrative. But it is the number that ties together later filings, ownership records, classification choices, payroll, banking, and change reporting. The IRS treats the EIN as the entity’s tax identity — and once it is issued, it does not move with the owner.

Any entity with an EIN must use Form 8822-B to report changes to the responsible party, address, or location. The IRS specifically requires responsible-party changes to be reported within 60 days. That is a deadline most founders never hear about — until the IRS notice arrives at the wrong address.

When founders treat EIN setup as clerical trivia, they tend to miss the chain that comes after it: who the IRS recognizes, what tax classification the application reflected, whether the LLC later changed structure, and whether the paperwork stayed consistent. Good accounting services to small business owners catch these threads early — not after a tax problem shows up.

Where DIY EIN Applications Most Often Go Wrong

Across foreign-owned LLC engagements, the same EIN-related mistakes show up repeatedly when founders self-apply or rely on formation services:

- Trying to use the IRS online EIN tool from outside the U.S. — it will not work, and time is wasted before discovering the international-applicant rule.

- Letting a formation agent list themselves as the responsible party — creating an IRS record that doesn’t match the actual owner.

- Leaving line 7b blank when the responsible party has no SSN or ITIN, instead of writing “foreign.”

- Selecting the wrong reason for applying on the SS-4 (e.g., “started new business” when the actual driver is Form 5472 reporting).

- Selecting the wrong entity classification on the SS-4 — which can lock the LLC into an unintended tax treatment until corrected.

- Failing to file Form 8822-B within 60 days when the responsible party changes.

- Applying for a second EIN when the original one would have worked — creating duplicate records the IRS has to reconcile.

Need help applying for an EIN from outside the U.S.? Optimize Tax LLC helps international founders with Form SS-4 filings, responsible-party corrections, Form 5472 compliance, and foreign-owned LLC reporting and taxes.

When Professional Help Is Worth the Investment

If any of these apply, professional help on the EIN application is strongly recommended:

- The LLC will be a foreign-owned U.S. disregarded entity filing Form 5472.

- The responsible party has no U.S. SSN or ITIN.

- The structure includes multiple foreign-owned LLCs or a foreign parent company.

- The LLC will elect corporate tax treatment via Form 8832 (timing matters).

- A formation agent already filed an EIN application with incorrect information that needs to be corrected.

- The original EIN was issued years ago and the responsible party or address has since changed.

Frequently Asked Questions

[DEV NOTE: Add FAQPage JSON-LD schema with @type FAQPage containing all 11 Q&A pairs as mainEntity array. See pillar page final_form_5472_conversational_cpa.html lines 60-96 for reference format.]

Does every foreign-owned LLC need an EIN?

Almost always, yes. If the LLC will file Form 5472, hire employees, owe excise tax, open a U.S. bank account, or operate as a multi-member LLC filing Form 1065, an EIN is required. The IRS also allows an EIN to be requested for banking purposes alone.

Can I apply for an EIN online from outside the U.S.?

No. The IRS online EIN tool requires the principal place of business to be in the U.S. or U.S. territories. International applicants must use Form SS-4 by phone, fax, or mail.

What number do international applicants call to get an EIN?

267-941-1099, Monday through Friday. The IRS may issue the EIN on the call and then request a signed Form SS-4 by fax or mail within 24 hours.

Do I need an ITIN before I can get an EIN for my LLC?

No. The SS-4 instructions allow the responsible party to enter “foreign” on line 7b if they do not have and are ineligible for an SSN or ITIN. A value must be entered — the line cannot be left blank.

Can a formation agent or registered agent be the responsible party?

Generally, no. The IRS defines the responsible party as the person who ultimately owns or controls the entity or its funds. Nominee services and formation agents typically don’t qualify.

How long does it take to get an EIN as an international applicant?

By phone: same day. By fax: about 4 business days (with a return fax number on the SS-4). By mail: 4–6 weeks. Phone is the fastest path for foreign applicants.

Can a non-U.S. resident apply for an EIN for an LLC?

Yes. Non-U.S. residents can apply for EIN LLC registrations using Form SS-4. Most international applicants request EIN for a foreign owned LLC by phone, fax, or mail because the online EIN system is generally unavailable to foreign applicants.

Can I apply for EIN LLC paperwork without an SSN?

Yes. The IRS instructions for Form SS-4 generally allow foreign applicants to enter “foreign” on line 7b if they do not have and are not eligible for an SSN or ITIN.

How long does it take to request EIN for a foreign owned LLC?

International applicants may receive an EIN the same day by phone. Fax applications commonly take around 4 business days, while mailed Form SS-4 applications may take several weeks.

Do I need a new EIN if my LLC changes ownership or structure?

Sometimes. The IRS has specific “when to get a new EIN” rules. A change in responsible party usually does not require a new EIN, but it must be reported on Form 8822-B within 60 days. Major structure changes (e.g., LLC to corporation) may require a new EIN.

What’s the difference between an EIN and an ITIN?

An EIN identifies a business for tax filing and reporting. An ITIN identifies an individual non-U.S. taxpayer who needs to file a U.S. tax return. Foreign founders often need both — an EIN for the LLC and an ITIN for the owner if they have a personal U.S. filing obligation.

For many international founders, the EIN becomes the foundation for foreign-owned LLC reporting and taxes in the United States. Getting the Form SS-4 filing correct from the beginning can help prevent future IRS compliance issues, reporting mismatches, and banking delays.

Get Your Free Compliance Calendar at Optimize Tax LLC

Use our free Compliance Calendar to get deadline reminders 30 days in advance – so the IRS never catches you off guard.

Your EIN is just the starting line. Next comes Form 5472, pro forma 1120, possible state filings, and annual report deadlines – all with their own due dates and penalties.

Got Your EIN? Know What Is Due Next.

The Bottom Line

A foreign-owned LLC does not become compliant because it exists. It becomes compliant when the identity on paper matches the reality of who owns it, how it is taxed, and what it is required to file.

The EIN is small, but it is usually the first moment the IRS asks you to get that story straight. Get it right at the start, and the rest of the compliance stack — Form 5472, Form 1065, 1040-NR, 1120-F — has somewhere clean to attach to.

Need Help Getting Your EIN — or Fixing One That Was Done Wrong?

Optimize Tax LLC works with foreign founders on the full setup stack — EIN applications via SS-4 (phone, fax, and mail), responsible-party guidance, ITIN applications when needed, and Form 8822-B updates to fix prior records.

If you are not sure whether your existing EIN was set up correctly — or you need a credentialed CPA and EA to handle the application from outside the U.S. — schedule a consultation at optimizetax.io.

Continue Reading: The Form 5472 Knowledge Series

- Foreign-Owned LLC Form 5472 Filing Guide

- Do I Need to File Form 5472 If My LLC Had No Activity?

- Foreign-Owned SMLLC Tax Filing Guide (2026)

- Form 8832 Entity Classification Election

- Form 1065 Filing Rules for Foreign-Owned Multi-Member LLCs

- Money Transfers Between Foreign-Owned LLCs: When the IRS Wants a Report

About the Author

Krishnaveni Raghavan, CPA, EA, is a Certified Public Accountant and IRS-credentialed Enrolled Agent with deep experience in U.S. tax compliance for foreign-owned LLCs, multi-entity structures, expats, and cross-border businesses. She regularly assists international founders who need to apply for EIN LLC filings, correct responsible-party records, and manage foreign-owned LLC reporting and taxes across complex cross-border structures. She leads the international tax practice at Optimize Tax LLC, where she advises on EIN and ITIN applications for foreign founders, entity classification (Form 8832), Form 5472 and pro forma 1120 filings, partnership withholding (Forms 8804/8805/8813), Forms 1040-NR and 1120-F, and IRS penalty resolution. As both a CPA and EA, she is licensed to represent taxpayers before the IRS in all 50 states.