Key Takeaways

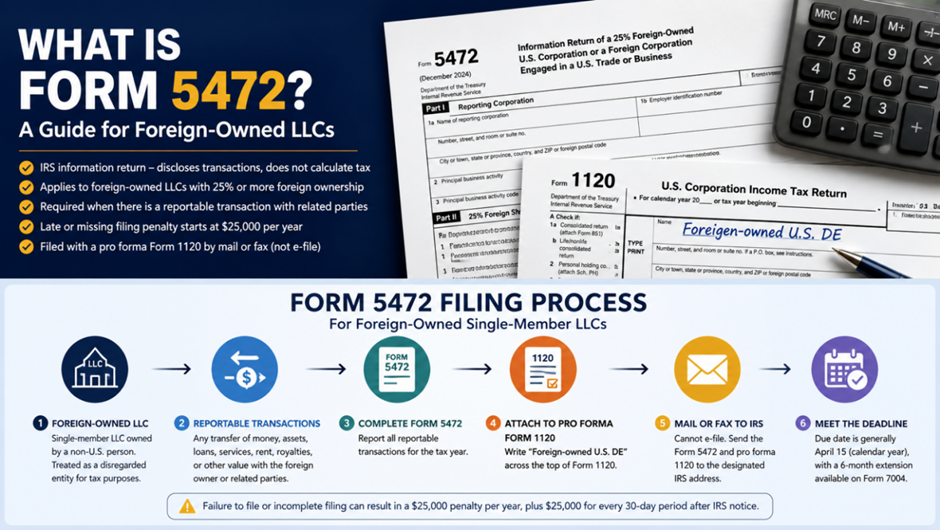

- Form 5472 is an IRS information return — it discloses transactions, it does not calculate tax.

- It applies to 25% foreign-owned U.S. corporations and to foreign-owned U.S. single-member LLCs (treated as disregarded entities for income tax).

- The form is required when a reportable transaction occurs between the LLC and its foreign owner or another related party — not just when the LLC earns revenue.

- The penalty for late, missing, or incomplete filing starts at $25,000 and can compound after IRS notice.

- Most foreign-owned single-member LLCs file Form 5472 attached to a pro forma Form 1120 — by mail or fax, not e-file.

- Multi-member LLCs taxed as partnerships generally do not file Form 5472, but face a different international reporting stack.

Most foreign founders discover Form 5472 the same way — well after the LLC is formed, the bank account is open, and a few transactions have already moved through it. Sometimes the discovery comes from a CPA. Sometimes it comes from an IRS penalty notice. Either way, the next question is the same:

“What exactly is Form 5472, and why does my single-member LLC have a $25,000 form attached to it?”

This guide is the plain-English answer to what is Form 5472. It is the entry point to the topic — the deeper scenario-specific guides are linked throughout for the situations that need more detail.

What Is Form 5472? (The 60-Second Answer)

Form 5472 is an IRS information return used to report transactions between a U.S. business and its foreign owner or other related parties. It applies to 25% foreign-owned U.S. corporations, foreign corporations engaged in a U.S. trade or business, and — most importantly for foreign founders — foreign-owned U.S. single-member LLCs treated as disregarded entities for income tax purposes.

It is not a tax return. It does not calculate income tax. Its purpose is disclosure. The IRS uses Form 5472 to see how money, assets, loans, services, and other value moved between the LLC and its foreign owner during the year.

Important: a foreign-owned LLC can have zero federal income tax liability and still have a Form 5472 filing obligation. The IRS is not asking what you owe. It is asking what moved.

Why the LLC Structure Triggers This in the First Place

Foreign entrepreneurs choose U.S. LLCs because they are fast to form, flexible, and operationally clean — you can open payment accounts, sign contracts, and run a business without the formalities of a larger corporate entity.

But the moment a foreign person owns 25% or more of a U.S. reporting corporation — or the moment a single-member LLC is treated as a foreign-owned U.S. disregarded entity under Section 6038A — the IRS may require Form 5472 (with a pro forma Form 1120) for that year. The U.S. government wants a record of the financial relationship between the company and its foreign owner. That is the entire purpose of the form.

Who Actually Has to File Form 5472

Form 5472 generally applies to:

- A 25% foreign-owned U.S. corporation — including S-corps and C-corps.

- A foreign corporation engaged in a U.S. trade or business.

- A foreign-owned U.S. single-member LLC, treated as a disregarded entity for income tax purposes under IRS Form 5472 requirements.

It generally does not apply to multi-member LLCs taxed as partnerships, which file Form 1065 instead — although those entities can face their own international reporting obligations through Section 1446 withholding (Forms 8804/8805), Schedules K-2/K-3, and other forms.

| Going Deeper — Entity Classification Matters First If your entity is a multi-member LLC, an LLC that elected corporate treatment, or a structure with foreign partners, the filing path is different. Read the dedicated guide: → Do Partnerships Need to File Form 5472? |

What Counts as a Reportable Transaction (At a High Level)

This is where most foreign founders get the rule wrong. Reportable transactions are not limited to large corporate transfers or sophisticated cross-border deals. They include the small, ordinary movements between an LLC and its foreign owner.

Common reportable transactions include money flowing into or out of the LLC, loans, payments for services, rent, royalties, reimbursements, and even the transactions involved in forming or dissolving the entity itself.

The pattern: if value moved between the LLC and its foreign owner — in either direction, in any amount — the IRS likely treats it as reportable under foreign-owned LLC Form 5472 rules. There is no de minimis exception.

| Going Deeper — What If My LLC Did Almost Nothing? The exception for “no reportable transactions” is real but narrower than founders expect. The dedicated guide walks through what truly qualifies, with a four-question self-test: → Do I Need to File Form 5472 If My LLC Had No Activity?

|

How and When You File Form 5472

For foreign-owned U.S. single-member LLCs, the Form 5472 filing package is specific:

- Form 5472 is attached to a pro forma Form 1120 (the corporate income tax return).

- “Foreign-owned U.S. DE” must be written across the top of the Form 1120.

- The package cannot be e-filed — it must be mailed or faxed to a dedicated IRS address.

- The deadline follows the Form 1120 due date — generally April 15 for calendar-year filers, with a six-month extension available via Form 7004.

These procedural rules are where most DIY filers slip up. A misrouted return is treated, for penalty purposes, as if it were never filed at all.

| Going Deeper — Step-by-Step Filing Guide For the full procedural walkthrough — entity setup, the seven filing steps, deadlines, extension routing, and how the owner’s personal return (1040-NR or 1120-F) fits in: → How to File Taxes for a Foreign-Owned Single-Member LLC (2026 Step-by-Step) |

The $25,000 Penalty Is Not Theoretical

The Form 5472 late filing penalty starts at $25,000 per year for failure to file or for filing a substantially incomplete or inaccurate form. If the failure continues after the IRS issues a notice, additional $25,000 penalties apply for every 30-day period.

The IRS does not soften this for small or dormant LLCs. It softens it for reasonable cause — and reasonable cause is much harder to argue once a notice has been issued. The leverage is in filing before the IRS asks.

A Simple Example That Explains the Whole Problem

A non-U.S. resident owns 100% of a U.S. single-member LLC. She opens the company in May, transfers $15,000 in to fund operations, pays for software and a contractor, and withdraws some money in December.

To her, that is ordinary startup movement. To the IRS, those are related-party transactions — which means a foreign-owned LLC Form 5472 requirement, regardless of whether the LLC made a profit.

If she ignores it until the penalty bill arrives, the cost of fixing it is real.

Three Mistakes That Cost Foreign Founders the Most

- Assuming “no revenue” means “no filing” — the IRS measures transactions, not income.

- Treating the LLC as a state-only matter — federal information reporting is separate.

- Reconstructing the year from screenshots in April — by then, gaps and missing records create their own problems.

When Professional Help Is Worth the Investment

Form 5472 is structurally simple. The penalty math, classification rules, mailing requirements, and owner-level return interactions are not. A credentialed accounting and taxation service for foreign-owned entities adds the most value when:

- You are filing for the first time and want it done right from year one.

- You missed prior years and need a careful catch-up filing strategy.

- You already received an IRS notice or penalty assessment.

- Your structure includes multiple related parties, entity classification elections, or non-cash transactions.

Frequently Asked Questions

What is Form 5472 in plain English?

Form 5472 is an IRS disclosure form that reports transactions between a U.S. business and its foreign owner or related parties. It is an information return — it does not calculate any tax.

Who has to file Form 5472?

Generally, 25% foreign-owned U.S. corporations, foreign corporations engaged in a U.S. trade or business, and foreign-owned U.S. single-member LLCs treated as disregarded entities.

Is Form 5472 a tax return?

No. It is an information return filed alongside a pro forma Form 1120 (for foreign-owned disregarded entities) or with a regular corporate return (for foreign-owned U.S. corporations).

What is the penalty for late filing?

$25,000 per year for failure to file or for filing a substantially incomplete return, plus an additional $25,000 for every 30-day period the failure continues after IRS notice. There is no statutory cap.

Can I e-file Form 5472?

Not for foreign-owned U.S. disregarded entities. The package must be mailed or faxed to a dedicated IRS address.

Do partnerships file Form 5472?

Generally, no. Partnerships file Form 1065 instead, with potential Section 1446 withholding obligations on top.

The Bottom Line

Form 5472 is not a paperwork nuisance. It is the IRS’s line of sight into foreign ownership and the financial movement that comes with it. For a foreign-owned LLC, the smartest move is not discovering the form after the deadline passes — it is building the LLC’s compliance rhythm into the business model from day one.

When the penalty notice arrives, the LLC stops being a simple structure very quickly.

| Need Help With Your Form 5472 Filing? Optimize Tax LLC works with foreign founders of U.S. LLCs every filing season — from first-year compliance and pro forma 1120 packages to multi-year catch-up filings, penalty-relief letters, and owner-level 1040-NR or 1120-F returns. Get expert help with your Form 5472 filing and avoid costly mistakes by scheduling a consultation today. |

Continue Reading: The Form 5472 Knowledge Series

This pillar guide covers the fundamentals. For the scenario that matches your situation, continue with:

- Do I Need to File Form 5472 If My LLC Had No Activity? — the deep dive on “inactive” years and the no-reportable-transaction exception.

- How to File Taxes for a Foreign-Owned Single-Member LLC (2026 Step-by-Step) — the full seven-step procedural walkthrough.

- Do Partnerships Need to File Form 5472? — how entity classification (single-member, multi-member, corporate election) changes the answer.

About the Author

Krishnaveni Raghavan, CPA, EA, is a Certified Public Accountant and IRS-credentialed Enrolled Agent with deep experience in U.S. tax compliance for foreign-owned LLCs, expats, and cross-border businesses. She leads the international tax practice at Optimize Tax LLC, where she advises foreign founders on entity structuring, Form 5472 and pro forma 1120 filings, partnership withholding (Forms 8804/8805), Forms 1040-NR and 1120-F, and IRS penalty resolution. As both a CPA and EA, she is licensed to represent taxpayers before the IRS in all 50 states.

Sources & References

- IRS Instructions for Form 5472 — Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business.

- IRS Form 1120 — U.S. Corporation Income Tax Return (used as pro forma for foreign-owned DEs).

- IRS Form 7004 — Application for Automatic Extension of Time to File Certain Business Income Tax, Information, and Other Returns.

- Internal Revenue Code § 6038A — Information with respect to certain foreign-owned corporations.

- Internal Revenue Code § 6038C — Information with respect to foreign corporations engaged in U.S. business.

- Treasury Regulations § 1.6038A-1 — General requirements (including 2017 extension to foreign-owned U.S. disregarded entities).